Monday, January 23, 2012

Greece Lines Up Portugal

By Delusional Economics, who is horrified at the state of economic commentary in Australia and is determined to cleanse the daily flow of vested interests propaganda to produce a balanced counterpoint. Cross posted from MacroBusiness.

Another weekend…. and we are still waiting for an outcome on Greece. The chief negotiators from Institute of International Finance (IIF) have left the country yet we still haven’t heard anything that sounds remotely like a deal. FT reports that the brinkmanship hasn’t ended but there doesn’t appear to be too much wiggle room left:

Lots of questions, but no real answers at this stage. What we do know is that Greece has a €14.5bn bond payment on 20 March and to meet this obligation it almost certainly needs another bailout. If the PSI deal is not completed quickly (possibly by the next EU summit on the 30th of Jan) then Greece will not get the additional support it requires and will therefore default in 2 months.

It is true that 2 months is a very long time in European economics so anything could happen between now and then, but the outcome of Greece, either way, is adding pressure on to the other weak links of Europe, such as Portugal:

I am not sure that “peril” is the correct word, but there is no doubt the outcome of Greece, one way or another, will have an effect on other periphery nations. This year Portugal enters its third year under a bailout and this year is expected to be the toughest with more tax hikes and the elimination of two months of pay for civil servants. The government is already calling for a economic contraction of 3%, but a look at the latest stats from the central bank suggest much worse.

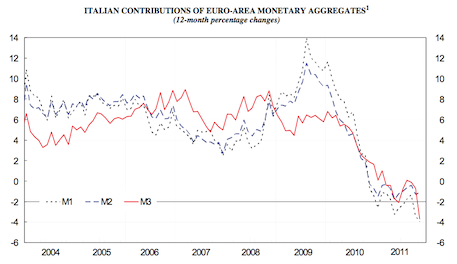

As we have seen in Italy, private sector deleveraging is accelerating led ,in part, by austerity government policy but also due to “zombification” of the banking system:

I also note that many economic indicators are heading in the wrong direction:

The Portuguese government did meet its obligations under its bailout agreement in 2011, but only by using a one-off transfer of money out of the banks’ pension funds to the government. In 2012 there is no backstop and therefore targets are unlikely to be met.

Over the weekend the government, with the final support of unions, introduced new reforms in an attempt to boost competitiveness including making it easier for employer to hire and fire staff, cutting holidays and severance pay requirements. It is yet to be seen if these changes can have an effect on the shrinking industrial output, but given the deleveraging environment this seems unlikely. Either way, the last thing the country needs at this point is a break-down in the Greek PSI talks that leads a further deterioration of trust in Europe’s periphery economics.

In other news Croatia wants in, Dexia is suing JP Morgan over mortgage securities and finally, Monti wants a trillion, the Germans want none of it, Draghi suggests something in the middle.

Another weekend…. and we are still waiting for an outcome on Greece. The chief negotiators from Institute of International Finance (IIF) have left the country yet we still haven’t heard anything that sounds remotely like a deal. FT reports that the brinkmanship hasn’t ended but there doesn’t appear to be too much wiggle room left:

Private owners of Greek debt have made their “maximum” offer for the losses they are willing to accept, the bondholders’ lead negotiator has said, implying that any further demands could kill off a “voluntary” deal and trigger a default.As I said last week, we will all just have to wait and see. There are many unknowns as to whether an initial deal can be struck and even if it can whether that will be enough. Is the rumoured 65-70% loss correct? Do the hedge funds have blocking position? Will Greece need to retrospectively apply a collective action clause to get a high participation rate? CDS triggers then? What about the ECB? Will the rest of the EU agree given they have a post-deal target of debt to GDP at 120%? Will there be any corresponding legal action?

Charles Dallara, managing director of the Institute of International Finance, said in an interview that he remained “hopeful and quite confident” the two sides could reach a deal that would prevent a full-scale Greek default when a €14.4bn bond comes due on March 20.

Lots of questions, but no real answers at this stage. What we do know is that Greece has a €14.5bn bond payment on 20 March and to meet this obligation it almost certainly needs another bailout. If the PSI deal is not completed quickly (possibly by the next EU summit on the 30th of Jan) then Greece will not get the additional support it requires and will therefore default in 2 months.

It is true that 2 months is a very long time in European economics so anything could happen between now and then, but the outcome of Greece, either way, is adding pressure on to the other weak links of Europe, such as Portugal:

Greece’s talks with creditors are currently proceeding under the rubric of a “voluntary” restructuring. Yet ratings agencies have stated unequivocally that anything other than the original bondholder terms will be classified as a technical default. Greece, Zervos says, will be “the first example in a developed market for how you deal with sovereign default.”All of which puts Portugal in a precarious spot. Most private investors have already fled the country’s bonds. But market observers say a Portuguese restructuring or default could still reverberate across Europe’s shaky banking sector, plunging the euro zone’s most vulnerable economies–and perhaps the entire global economy–into financial peril.

I am not sure that “peril” is the correct word, but there is no doubt the outcome of Greece, one way or another, will have an effect on other periphery nations. This year Portugal enters its third year under a bailout and this year is expected to be the toughest with more tax hikes and the elimination of two months of pay for civil servants. The government is already calling for a economic contraction of 3%, but a look at the latest stats from the central bank suggest much worse.

As we have seen in Italy, private sector deleveraging is accelerating led ,in part, by austerity government policy but also due to “zombification” of the banking system:

I also note that many economic indicators are heading in the wrong direction:

The Portuguese government did meet its obligations under its bailout agreement in 2011, but only by using a one-off transfer of money out of the banks’ pension funds to the government. In 2012 there is no backstop and therefore targets are unlikely to be met.

Over the weekend the government, with the final support of unions, introduced new reforms in an attempt to boost competitiveness including making it easier for employer to hire and fire staff, cutting holidays and severance pay requirements. It is yet to be seen if these changes can have an effect on the shrinking industrial output, but given the deleveraging environment this seems unlikely. Either way, the last thing the country needs at this point is a break-down in the Greek PSI talks that leads a further deterioration of trust in Europe’s periphery economics.

In other news Croatia wants in, Dexia is suing JP Morgan over mortgage securities and finally, Monti wants a trillion, the Germans want none of it, Draghi suggests something in the middle.

http://hat4uk.wordpress.com/2012/01/23/stand-off-in-athens-how-a-local-negotiation-turned-into-an-international-battle-for-survival/

STAND-OFF IN ATHENS: How a local negotiation turned into an international battle for survival.

As I struggled along with most other observers to work out just WTF had gone wrong in Athens last Saturday morning, The Slog’s only reliable source finally surfaced to say a thing or two. In the time since then, I have been trying to piece together what happened…with the help of the Bankfurt mole, and sources in Washington and Paris.

As I struggled along with most other observers to work out just WTF had gone wrong in Athens last Saturday morning, The Slog’s only reliable source finally surfaced to say a thing or two. In the time since then, I have been trying to piece together what happened…with the help of the Bankfurt mole, and sources in Washington and Paris.“This thing was snatched from our grasp yesterday [Friday] afternoon,” the Athens negotiator told me, “and removed to a much higher sphere. It could be that the EU finally grew some balls.”

The detail of what seems to have occurred must remain as conjecture until somebody writes a book about this saga. What’s clear is that last Friday around lunchtime, a deal had been reached for some low-start new bond issues, followed by later-maturing ones at a higher rate. In return for a 70% haircut by the lenders, the rate average of all the bonds to be issued was 4.25%. The legal beagles went away to write it up amid cautious handshakes. At which point some Troika heavies made an announcement: nope, the average had to be no more than 3%.

That was a big difference. But this wasn’t the Greeks making the demand: it was the IMF, the ECB, Berlin, a bit of Paris…and just a hint of Wolfgang Schauble – the all-time believer in default within the EU.

Somebody somewhere had decided that the time was right for a power play. Major offloaders of March-maturing bonds had been French and German banks in recent months….with targeted help from Draghi’s ECB. Whether this was a trap deliberately set by Draghi I couldn’t say, but either way its effect has been to leave Paris and Berlin considerably less exposed to Greek debt than previously….and the Hedgies holding the baby. By Saturday lunchtime, it had dawned on the key IIF movers that a point was being made from the top: “OK punks – let’s see what you got”.

Significantly, Merkel, Lagarde, van Rompuy and Barroso held a pow-wow in Berlin yesterday afternoon. There is a growing feeling that the EU ‘management’ now feels it is ready to face a default inside the eurozone. The point – and for once, it’s a sensible idea – would be to say to a frightened world, “Look – we rode a default, and won”.

If correct, this vindicates all those who have said from the start that Merkozy was simply playing for time with both the Greeks and their creditors: that once the banks had been sandbagged, they would turn round to the bondholders and say, “OK – do your worst”. It is an enormous gamble. If pushed too hard by their bondholders, Iberia and Italy might give up and default too; and that would make the euro too toxic to survive. But the opinion being followed is, “If we win in Greece, the lenders will back off in Spain”.

The Slog’s Frankfurt Maulwurf seems fairly happy at the turn of events. Here’s his version:

“Chancellor Merkel has come under enormous pressure in recent weeks from the German banking community, and also from her own [CDU] colleagues. The advice has been clear: unless we stop somewhere, the problems will go on and on and cost more and more – with only Germany left standing. There can be no doubt that Signor Draghi has helped in this regard….he has influence with [Merkel] and also he is more proactive than Trichet was in providing financial support in the right places. For the first time now, we see those trying to take advantage of our situation on the back foot. This can only be for the good of all Europeans”.

We have to remember in all this that our Bankfurt friend is very much a hawk in the ‘keep the EU affordable or walk away from it’ tendency. He is also firmly of the view that FiskalUnion is central to that:

“Where Draghi’s influence has been crucial is in keeping the French from diluting the rules of the Fiscal Pact. He is totally in accord with Frau Merkel on this. There is no doubt in my mind that the eurozone is in better shape to face the future than it was before Christmas”.

Whether that is really true remains something about which I’m deeply sceptical. Although Charles Dallara of the IIF continued to make nice noises from his appointment in Paris, some of the creditors involved in Friday’s shock-and-awe moment were talking about “drawing a line in the sand at 3.8% and saying take it or leave it”.

“I heard two guys say on Friday, ‘this is a deal-breaker’ – and they meant it,” says my Athens source. So we really do have a stand-off, and from here on it is the classic ‘who blinks first?’ situation. Early today I had input from Paris. I will give you the key paragraph:

“It isn’t just about the EU’s strength, it is also about the hopeless position of Greece. Their economic data gets worse by the month, and so the mountain they must climb gets steeper and steeper. Any expensive deal in Athens would simply be a stay of execution.”

But then – much as I love him – that source is a French diplomat. My feeling remains that the Brussels view on Greece is they are a concern only so long as they are a liability. And I still feel – no, I know – that only a 100% write-off of all its debt today (followed by an immediate injection of economic stimulation) would give the Greek People a fighting chance of survival within the single currency. Clearly, that isn’t going to happen.

“The elements of an unprecedented voluntary private-sector involvement are coming into place,” puffed Charles Dallara to Bloomberg yesterday. As Eric Morecambe might have said, “We have all the right elements…just not necessarily in the right order”.

EU REALITY CHECK -

UNCHANGED: STILL NO REALITY

Calling the IIF’s bluff over Greek debt is a bold move – but the fundamentals remain the same.

Wolfgang Schauble having stated clearly last Friday that there would be no doubling of the eventual ESM (the final post-July EU rescue fund) Chancellor Merkel reiterated this today in the German media. She would “listen to what other countries bring to the table”, and then act accordingly…by ignoring them.Mario Monti will thus not be best pleased, but personally, I’m incandescent with rage. Not about the ESM – which is at best a fart trying to counterbalance a typhoon – but at the continuing way in which Berlin and Paris (with input from the Italian in Frankfurt) continue quite brazenly now to treat the EU as their own little creation – a club with which they can do as they please.

There are 27 States in the EU, and they all have an equal vote. As long as that continues, of course, nothing will ever get done. But if you’re asking me to choose between a uselessly indecisive Superstate and a fascist authority run by a German and a banker, my vote goes for ‘neither of the above’. What it boils down to – and it always has – is that for all those Brits with enough brainpower to prefer keeping their freedoms and savings intact, the EU is and always was a non-starter. Once the Ezone came into being, its self-immolation became a certainty: but while we are doing the hokey-cokey here in the UK, somebody needs to tell the Westminster clique that the rest of us would prefer to depart the dance-floor and go home.

For example, if the Germans say ‘no dice’ on a doubled ESM, that snuffs any remaining, remote chance that Washington will give Frufru Lagarde any more ammo for her IMF bazooka. Frau Merkel’s morality play continues, but that’s all it is: a show that bears no connection to the real world.

Lagarde herself told a Berlin audience within the last hour that there should be “a temporary flexibility of monetary policy by the European Central Bank (ECB) to help the euro countries with poor access to financial markets” (flatly opposed by Merkel, and publicly discouraged by Mario Draghi) that “all EU countries must try harder to find funds to help their neighbours” (most of them can’t afford their own problem, let alone someone else’s) and that the ESM “must secure substantial additional resources” (see opening para above). As she and Merkel spent four hours talking to each other yesterday it’s pretty obvious there was little in the way of a meeting of minds….which is quite likely if one of you hasn’t got one at all.

Back in the real world, Spain is rapidly turning into Greece: it faces a contraction of 1.5% during 2012 according to its central bank, so given the normal 100% margin of error, we can expect 3% to be nearer the mark. This announcement will immediately increase its borrowing costs, and over the year these two factors will mean the country sinking deeper into the quicksand.

Le Monde this morning reports on the latest business survey, which unsurprisingly shows opinion becoming ‘increasingly morose’ on the subject of the economic outlook. Intriguingly, it has also just broken a sourced story saying that the IIF has said to the Troika, re Greek debt, ’70% haircut plus 4% coupon – final offer’. My own information is that they’d take 3.8%, but nobody really knows any more: if the bondholders call the Troika’s hand, however, things will get interesting in the Chinese sense.

Returning to the case of Greece, the economy has shrunk far more than experts had projected: it fell nearly 4% last year, and in 2012 is expected to contract by more than the 3% originally suggested by international observers. The country’s debt burden continues to climb – it’s now above 142%. So the Troika’s gamble begins to make more and more sense: it either wins this battle with the lenders, or…or what? Kicks Greece out of the euro? No. Leaves the euro? Quite possibly. Somewhere in New York and Athens, there are folks working round the clock to decide whether they’d rather give in on the haircut/coupon thing – and still take a very fat profit now; or push the Troika to the edge…and wait for an obscene profit if the triplets lose their nerve. I know what I’d do – but Hedge Funds don’t think like the rest of us.

In Portugal, every single bank lost money last year, but the Central Bank is rushing to reassure customers there is nothing to worry about, because the EU recapitalisation target of 9% has been met by all of them. And Lisbon’s Metro fares just went up 5% as part of the desperate search to empty the nation’s pockets in every conceivable way.

The above news is just a skimmed cross-section of EU-based newspapers I looked at this morning: all is muddle, disaster and disagreement.

Tell me, do you think anyone in Camerlot actually reads these papers at all?

2222222222222222222222

-

Bill Cunningham | World Unite

Here we go.

Cunningham has published something important.This could develop. -

Luckycharms

-

Does IMF Stand for Impressive Macroeconomic Flexibility?

So the IMF is holding a meeting on rethinking macroeconomic policy (I was invited but couldn’t make the timing work.) And the Fund’s chief economist has already made it clear that he’s open to some serious revision of the prevailing paradigm.

All money is debt.Bank debt or government debt makes no difference.A modest rate of inflation encourages investments that pay.Paying off debt destroys money.Taxes remove money from the economy.Destroying debt, bankruptcy, removes money from the economy.Bankruptcy is a another cure for inflation.

http://www.nytimes.com/pages/business/index.html

I.M.F. Chief Urges Europe to Beef Up Bailout Funds

By DAVID JOLLY

As euro zone finance ministers gathered in Brussels, the managing director of the International Monetary Fund said a "larger firewall" was needed to safeguard global financial stability.The Telegraph:

Debt crisis live: finance ministers meet as Greek debt talks stall

German Chancellor Angela Merkel rejects suggestions from the IMF, Italy and Spain that the size of its future bailout fund should be increased as eurozone finance ministers to decide if Greek has met bail-out terms.

23 Jan 2012| 205 CommentsDebt crisis: IMF chief warns of '1930s moment'

IMF head Christine Lagarde set out Monday a raft of proposals to fight the eurozone crisis, including a bigger rescue fund, lower ECB rates and eurobonds as she warned of dimmer world growth prospects.

23 Jan 2012| 3 CommentsGermany rejects calls for bigger eurozone bail-out fund

German Chancellor Angela Merkel has rejected suggestions from the IMF, Italy and Spain that the size of its future bailout fund should be increased.

23 Jan 2012| 5 CommentsSpanish central bank warns of double dip recession

Spain's central bank said the debt-laden country will fall back into recession this year with the economy contracting 1.5pc.

23 Jan 2012| 3 CommentsGreek debt deal: 'We've made our best offer', says banks

Banks holding Greek debt said they had made their best offer on restructuring talks and a deal now depends on whether EU-IMF bailout providers will budge on bond losses.

23 Jan 2012| 5 Comments -

-

GeniusIQ179

http://www.washingtonpost.com/national/health-science/documentary-reveals-how-contaminated-water-at-the-nations-largest-marine-base-damaged-lives/2012/01/10/gIQAfpy4GQ_story.html

Mike Partain didn’t believe the rumors about a place called Baby Heaven until he visited a Jacksonville, N.C., graveyard and wandered into a section where newborns were laid to rest.

Surrounded by hundreds of tiny marble headstones, he started to cry. A documentary film crew that followed him for a story about water contamination at Camp Lejeune heard his whimpers through a microphone clipped to his clothes. The crew dashed from another part of the graveyard and found him asking, “Why them and not me?”

222Comments- Weigh In

- Corrections?

The scene at Jacksonville City Cemetery is among the more poignant moments in the documentary “Semper Fi: Always Faithful,” about the men, women and children affected over three decades by contaminated water at the nation’s largest Marine base. The film made the short list of 15 documentary features being considered for an Oscar; the Academy of Motion Picture Arts and Sciences will cut the list to five Tuesday." . . . http://en.wikipedia.org/wiki/Camp_Lejeune_water_contamination

{kind=link}

. . . "In this case, the solution is to work on the language of the bills to rule out the sorts of abuses that the big Web sites fear. (And to fix the other minor point, which is that the bills won’t work. For example, they’d make American Internet companies block your access to domain names like “piracy.com,” but you’d still be able to get to them by typing their underlying numerical Internet addresses, like 197.12.34.56. In other words, anybody with any modicum of technical skills would easily sidestep the barriers.)

As it turns out, that’s exactly what’s happening. Dozens of members of Congress, and the White House itself, have dropped support of the bills; their sponsors are considering big changes to the proposals. (They might look, for starters, at the suggestions in Wednesday’s Times editorial: “The legislation could be further amended to narrow the definition of criminality and clarify that it is only aimed at foreign sites. And it could tighten guarantees of due process. Private parties must first get a court order to block business with a Web site they deem infringing on their copyrights.”)

In other words, the protests were effective. There’s no chance that the bills will become law in their current forms.

But it was a sloppy success; the scare language used by some of the Web sites was just as flawed as the Congressional language that they opposed. (I actually have sympathy — just a tiny bit — for the music business’s frustration. It was put nicely by Cary Sherman, chief executive of the Recording Industry Association of America: “It’s very difficult to counter the misinformation when the disseminators also own the platform.”)

Finally, not enough people have acknowledged that the opposition was arguing two totally different different points — the “you’re going about it the wrong way” group and the “we want our illegal movies!” group.

In the new world of Internet versus government, the system worked; the people spoke, government listened, and that’s good. But let’s do it responsibly, people. Both sides have an obligation to do the right thing."

.